Comerica Incorporated (NYSE:CMA) offers a high dividend yield, but this doesn’t seem to be enough to offset weakness in its operating performance.

As I’ve covered in previous articles, Comerica is one of the U.S. banks most geared to rates, a profile that theoretically was good during a rising interest rate environment, like the one experienced during 2022-23.

However, since my last article on Comerica back in March 2021, its shares are down by about 20% including dividends and have underperformed the U.S. banking sector, especially after March 2023 due to the banking turmoil in the regional banking sector.

As I’ve not covered Comerica for some time and the interest rate environment is expected to change in the future to a downward trajectory, I think it’s now a good time to revisit its investment case to see whether Comerica offers value for long-term investors or not.

Business Overview

Comerica is a regional bank that offers several financial services, including loans, treasury management and capital market solutions. It has operations in the U.S., mainly in Texas, California, and Michigan, plus an international presence in Mexico and Canada.

At the end of 2023, its total assets amounted to some $85 billion, being therefore a relatively small bank by this measure. Its shares are listed on the New York Stock Exchange and its current market value is about $6.4 billion.

Comerica’s business is spread under three main operating segments, namely Commercial Banking, Wealth Management, and Retail Banking. By loans, some 86% of its loans are generated in commercial banking, while wealth management accounts for 10%, and retail customers only for 4%. This is a different profile than most banks, which usually are more exposed to retail customers, even though on the deposit side its profile is more diversified and less geared to commercial banking.

Business mix (Comerica)

Geographically, while Comerica is present in several states, its three most important ones account for more than 80% of total loans and about 75% of deposits, which means its business is relatively concentrated in a few selected regions.

This is part of the bank’s strategy of being a “partner” to its commercial customers and offering a good customer service, something that would be more difficult to achieve if its operations were spread across more regions.

Regarding growth, the bank’s track record is not particularly impressive considering its loan book has been relatively stable at about $50 billion over the past few years, even though it was on an upward trajectory until the first quarter of 2023.

Indeed, Comerica’s business was progressing well until the banking industry in the U.S. was impacted by the collapse of Silicon Valley Bank and two other small regional lenders in the following months, which was a tough period for regional banks. Comerica was no exception, but its relationship business model was key to maintaining customer’s trust in its brand during this period of turmoil in the regional banking sector.

Given this backdrop, Comerica’s management took some strategic actions to strengthen its balance sheet and put even more focus on its relationship operating model, deciding to reduce wholesale funding, exiting the mortgage banker financing business, and reducing equity fund services with customers with whom it didn’t have much of a relationship.

This led to a lower loan book and deposits in recent quarters, which impacted negatively its financial performance, but given the banking turmoil in the regional sector during 2023, this seems to be sensible action by Comerica’s management to maintain a sound business model over the long term.

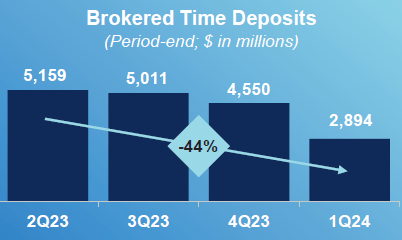

As seen in the next graph, its brokered time deposits declined considerably since the second quarter of 2023, reducing the bank’s exposure to wholesale funding and increasing the weight of deposits from its relationship customers, which should be more “sticky” over the long term. Despite this decline in brokered deposits, at the end of last March, its total deposits amounted to about $65 billion (-3.7% YoY) and its loan-to-deposits ratio was 80%, a level that is close to the average of its peers.

Brokered deposits (Comerica)

Despite the banking turmoil in 2023, Comerica’s strategy has not changed much, and the bank remains focused on having a stable business over the long term, maintaining sound loan underwriting criteria and not being much focused on increasing risk in its balance sheet. While this strategy may not lead to much business growth in the coming years, it’s positive for asset quality and for Comerica to maintain below-average credit losses in the future.

Financial Overview

Regarding its financial performance, Comerica’s track record can be considered mixed over the past few years, as the bank has a good operating leverage related to rates, leading to a higher top-line, but due to higher expenses this has not translated into higher net income compared to the period when rates were close to zero.

Indeed, Comerica is one of the banks with higher leverage to rates due to its business mix, with above-average non-interest bearing deposits, while on the asset side it has a good share of loans with variable rates. This profile is quite positive during a rising interest rate environment, like the one experienced during 2022-23.

Not surprisingly, its net interest income increased from about $1.8 billion in 2021 to more than $2.5 billion in 2023, representing an increase of around 39% in two years. On the other hand, its non-interest income declined a little bit during this period ($1.07 billion in 2023 vs. $1.1 billion in 2021), thus its revenue growth over the past couple of years was all related to higher rates.

Theoretically, this should have been a significant boost for its bottom-line and profitability, but there were some offsetting effect that led to a lower net income in 2023 compared to 2021. First, provisions for loan losses were negative in 2021 by some $384 million (which means the bank made reversals following the big jump in 2020 related to the pandemic), while over the past couple of years its provisions were more ‘normal’ at $60 million in 2022 and $89 million.

Therefore, while net interest income increased by $700 million in two years, the difference in provisions for loan losses impacted negatively its bottom-line by $473 million in 2023 compared to 2021.

Another issue that also had a great impact in its profitability was the inflationary environment, which put pressure on staff costs, leading to overall expenses of $2.36 billion in 2023, compared to $1.86 billion in 2021 (+27% in two years). This is a difference of about $500 million, which wiped out Comerica’s gain from higher rates.

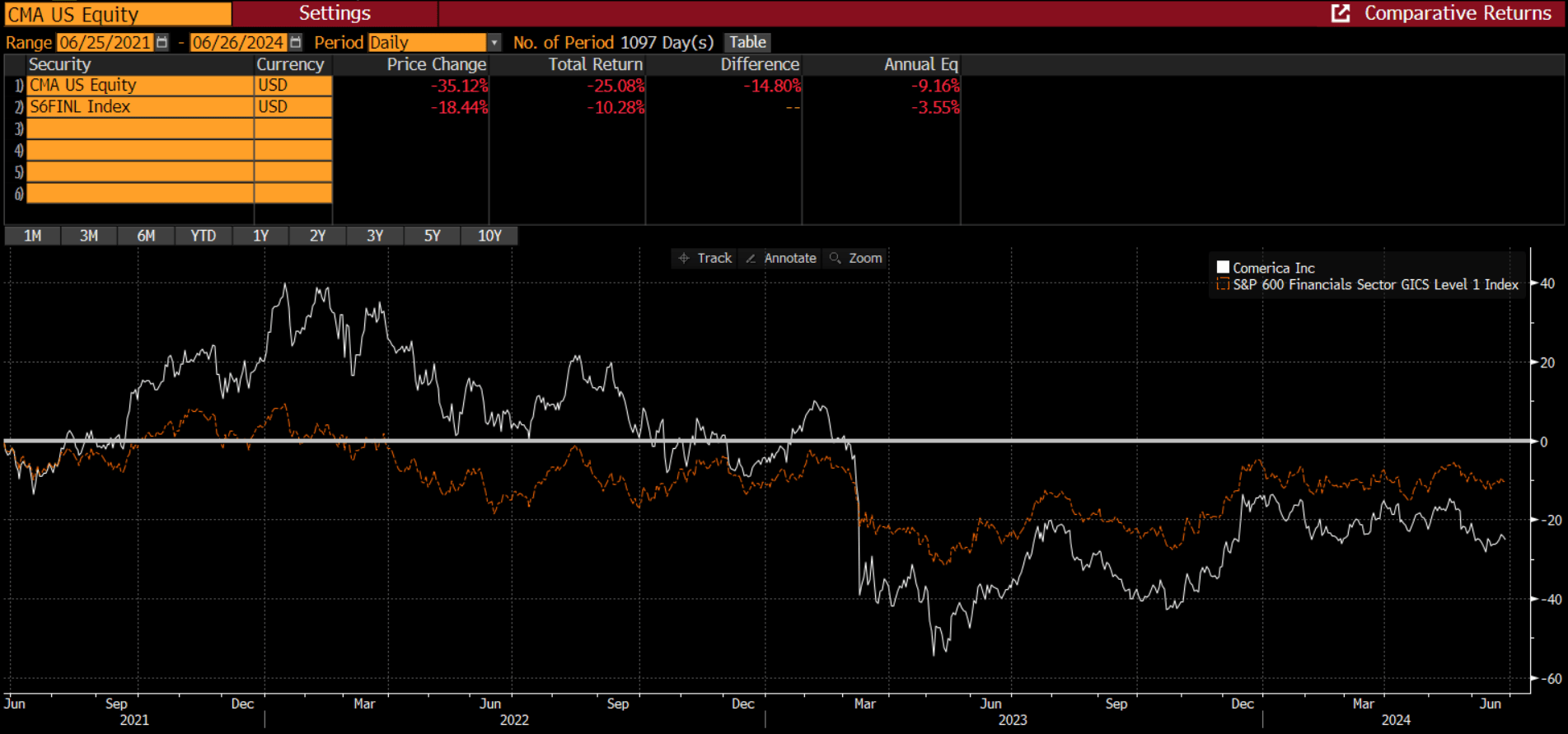

Taking this background into account, Comerica’s net profit last year was only $854 million (vs. $1.1 billion in 2021), which is an unexpected outcome considering how rapid rates have increased between 2022 and the middle of 2023. This relatively weak performance justifies, in my opinion, to a large extent, Comerica’s negative share price performance over the past three years, underperforming the banking sector during this period, as shown in the next image.

Share price performance (Bloomberg)

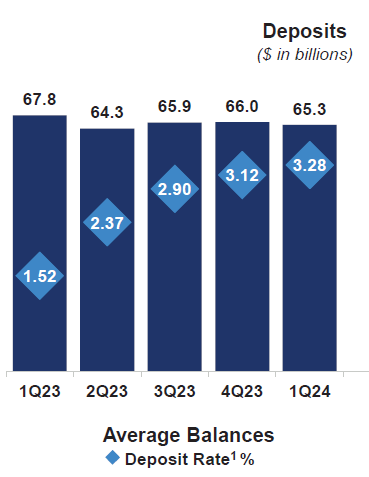

During the first quarter of 2024, its operating momentum has not improved much, given that a lower loan book and higher cost of deposits led to declining net interest income in the quarter. Indeed, its loan book declined by 2.7% YoY and deposits were down by 1.1% YoY, but what impacted most the bank’s net interest income was a higher cost of deposits, which increased to 3.28% on average in Q1 2024.

This is a much higher cost of deposits than in the same quarter of 2023 (1.52%), showing that the banking turmoil following Silicon Valley’s collapse had a great impact on Comerica’s business. Like its peers, to avoid significant deposit outflows, the bank had to increase deposit rates, leading to a much higher deposit beta than historically had. Given that Comerica’s core business is taking deposits and making loans, it’s natural to see that this affected greatly its financial performance, and this trend is not easy to reverse in the short term.

Deposits (Comerica)

Given this background, it’s not surprising that Comerica’s net interest income declined to $548 million in Q1 2024, a decline of 22.6% YoY, and its net interest margin declined to 2.80% (vs. 3.57% in Q1 2023).

Regarding costs, they continued to be impacted by higher staff expenses and contributions to FDIC insurance, increasing to $603 million in Q1 2024 (+9.4% YoY), leading to an efficiency ratio of 77% in the quarter. This is not a good efficiency level and is much higher than the best banks in the U.S., which are below 60%, showing that Comerica’s top-line momentum is impacting quite negatively its fundamentals.

On the other hand, its asset quality remains excellent despite its relatively high exposure to commercial customers and some exposure to commercial real estate, showing that its underwriting criteria is sound, and credit losses should remain low in the near future. Despite that, its net income in the quarter was only $138 million, a decline of 57% YoY, and its return on equity (ROE) ratio was 9.3% (vs. 24% in Q1 2023).

Going forward, the bank’s operating performance, according to analysts’ estimates, is not expected to improve much in the coming quarters with net interest income expected to be around $2.2 billion in 2024 (-12% YoY) and its net income should drop to less than $700 million in the year (-22% YoY). This means Comerica’s financial performance is not particularly impressive in the short term, despite the “higher for longer” rate environment.

Given that the bank is highly exposed to rates, if the Federal Reserve eventually starts to cut interest rates in the coming months, Comerica’s business will certainly be impacted and its decline in revenues and earnings could be even worse.

While the bank hedges to some extent its exposure to rates through interest-rate swaps, its sensitivity to rates is still significant and Comerica’s top-line is likely to be pressured by the end of 2024 or 2025, if rates decline as expected nowadays by the street. Investors should not that current consensus is for the Fed to

Detroit, Michigan – Comerica Incorporated, a regional bank headquartered in Dallas, continues to face challenges despite offering a high dividend yield. Known for its focus on interest rates, the bank’s operating performance has been underwhelming, leading to a decline in its share price over the past year.

Comerica’s business spans across multiple states, with a significant presence in Texas, California, and Michigan, as well as international operations in Mexico and Canada. While the bank boasts total assets of around $85 billion, making it a relatively small player in the industry, its market value stands at approximately $6.4 billion.

The bank’s business is divided into three main segments: Commercial Banking, Wealth Management, and Retail Banking. Unlike traditional banks, Comerica generates the majority of its loans from commercial banking rather than retail customers. This unique profile has both advantages and challenges in terms of diversification and growth opportunities.

In response to recent industry challenges, Comerica’s management has taken strategic actions to strengthen its balance sheet and focus on its relationship-driven operating model. This includes reducing wholesale funding, exiting certain businesses, and prioritizing customer relationships over short-term gains.

Despite a resilient business model, Comerica’s financial performance has been impacted by external factors such as the collapse of Silicon Valley Bank and increased competition in the regional banking sector. The bank’s net interest income has declined, leading to lower profitability and a cautious outlook for future earnings.

Looking ahead, analysts forecast continued pressure on Comerica’s financial performance, with net interest income expected to decrease in the coming quarters. The bank’s exposure to interest rates poses a significant risk, especially if the Federal Reserve decides to cut rates, further impacting revenues and earnings.

While Comerica remains well-capitalized with a strong dividend yield, investors should exercise caution given the bank’s challenging operating environment. With uncertainties surrounding future interest rate movements, Comerica’s shares may face additional headwinds in the near term. As such, some analysts recommend a cautious approach when considering investment opportunities in the bank.

Comerica Incorporated (NYSE:CMA) offers a high dividend yield, but this doesn’t seem to be enough to offset weakness in its operating performance.

As I’ve covered in previous articles, Comerica is one of the U.S. banks most geared to rates, a profile that theoretically was good during a rising interest rate environment, like the one experienced during 2022-23.

However, since my last article on Comerica back in March 2021, its shares are down by about 20% including dividends and have underperformed the U.S. banking sector, especially after March 2023 due to the banking turmoil in the regional banking sector.

As I’ve not covered Comerica for some time and the interest rate environment is expected to change in the future to a downward trajectory, I think it’s now a good time to revisit its investment case to see whether Comerica offers value for long-term investors or not.

Business Overview

Comerica is a regional bank that offers several financial services, including loans, treasury management and capital market solutions. It has operations in the U.S., mainly in Texas, California, and Michigan, plus an international presence in Mexico and Canada.

At the end of 2023, its total assets amounted to some $85 billion, being therefore a relatively small bank by this measure. Its shares are listed on the New York Stock Exchange and its current market value is about $6.4 billion.

Comerica’s business is spread under three main operating segments, namely Commercial Banking, Wealth Management, and Retail Banking. By loans, some 86% of its loans are generated in commercial banking, while wealth management accounts for 10%, and retail customers only for 4%. This is a different profile than most banks, which usually are more exposed to retail customers, even though on the deposit side its profile is more diversified and less geared to commercial banking.

Business mix (Comerica)

Geographically, while Comerica is present in several states, its three most important ones account for more than 80% of total loans and about 75% of deposits, which means its business is relatively concentrated in a few selected regions.

This is part of the bank’s strategy of being a “partner” to its commercial customers and offering a good customer service, something that would be more difficult to achieve if its operations were spread across more regions.

Regarding growth, the bank’s track record is not particularly impressive considering its loan book has been relatively stable at about $50 billion over the past few years, even though it was on an upward trajectory until the first quarter of 2023.

Indeed, Comerica’s business was progressing well until the banking industry in the U.S. was impacted by the collapse of Silicon Valley Bank and two other small regional lenders in the following months, which was a tough period for regional banks. Comerica was no exception, but its relationship business model was key to maintaining customer’s trust in its brand during this period of turmoil in the regional banking sector.

Given this backdrop, Comerica’s management took some strategic actions to strengthen its balance sheet and put even more focus on its relationship operating model, deciding to reduce wholesale funding, exiting the mortgage banker financing business, and reducing equity fund services with customers with whom it didn’t have much of a relationship.

This led to a lower loan book and deposits in recent quarters, which impacted negatively its financial performance, but given the banking turmoil in the regional sector during 2023, this seems to be sensible action by Comerica’s management to maintain a sound business model over the long term.

As seen in the next graph, its brokered time deposits declined considerably since the second quarter of 2023, reducing the bank’s exposure to wholesale funding and increasing the weight of deposits from its relationship customers, which should be more “sticky” over the long term. Despite this decline in brokered deposits, at the end of last March, its total deposits amounted to about $65 billion (-3.7% YoY) and its loan-to-deposits ratio was 80%, a level that is close to the average of its peers.

Brokered deposits (Comerica)

Despite the banking turmoil in 2023, Comerica’s strategy has not changed much, and the bank remains focused on having a stable business over the long term, maintaining sound loan underwriting criteria and not being much focused on increasing risk in its balance sheet. While this strategy may not lead to much business growth in the coming years, it’s positive for asset quality and for Comerica to maintain below-average credit losses in the future.

Financial Overview

Regarding its financial performance, Comerica’s track record can be considered mixed over the past few years, as the bank has a good operating leverage related to rates, leading to a higher top-line, but due to higher expenses this has not translated into higher net income compared to the period when rates were close to zero.

Indeed, Comerica is one of the banks with higher leverage to rates due to its business mix, with above-average non-interest bearing deposits, while on the asset side it has a good share of loans with variable rates. This profile is quite positive during a rising interest rate environment, like the one experienced during 2022-23.

Not surprisingly, its net interest income increased from about $1.8 billion in 2021 to more than $2.5 billion in 2023, representing an increase of around 39% in two years. On the other hand, its non-interest income declined a little bit during this period ($1.07 billion in 2023 vs. $1.1 billion in 2021), thus its revenue growth over the past couple of years was all related to higher rates.

Theoretically, this should have been a significant boost for its bottom-line and profitability, but there were some offsetting effect that led to a lower net income in 2023 compared to 2021. First, provisions for loan losses were negative in 2021 by some $384 million (which means the bank made reversals following the big jump in 2020 related to the pandemic), while over the past couple of years its provisions were more ‘normal’ at $60 million in 2022 and $89 million.

Therefore, while net interest income increased by $700 million in two years, the difference in provisions for loan losses impacted negatively its bottom-line by $473 million in 2023 compared to 2021.

Another issue that also had a great impact in its profitability was the inflationary environment, which put pressure on staff costs, leading to overall expenses of $2.36 billion in 2023, compared to $1.86 billion in 2021 (+27% in two years). This is a difference of about $500 million, which wiped out Comerica’s gain from higher rates.

Taking this background into account, Comerica’s net profit last year was only $854 million (vs. $1.1 billion in 2021), which is an unexpected outcome considering how rapid rates have increased between 2022 and the middle of 2023. This relatively weak performance justifies, in my opinion, to a large extent, Comerica’s negative share price performance over the past three years, underperforming the banking sector during this period, as shown in the next image.

Share price performance (Bloomberg)

During the first quarter of 2024, its operating momentum has not improved much, given that a lower loan book and higher cost of deposits led to declining net interest income in the quarter. Indeed, its loan book declined by 2.7% YoY and deposits were down by 1.1% YoY, but what impacted most the bank’s net interest income was a higher cost of deposits, which increased to 3.28% on average in Q1 2024.

This is a much higher cost of deposits than in the same quarter of 2023 (1.52%), showing that the banking turmoil following Silicon Valley’s collapse had a great impact on Comerica’s business. Like its peers, to avoid significant deposit outflows, the bank had to increase deposit rates, leading to a much higher deposit beta than historically had. Given that Comerica’s core business is taking deposits and making loans, it’s natural to see that this affected greatly its financial performance, and this trend is not easy to reverse in the short term.

Deposits (Comerica)

Given this background, it’s not surprising that Comerica’s net interest income declined to $548 million in Q1 2024, a decline of 22.6% YoY, and its net interest margin declined to 2.80% (vs. 3.57% in Q1 2023).

Regarding costs, they continued to be impacted by higher staff expenses and contributions to FDIC insurance, increasing to $603 million in Q1 2024 (+9.4% YoY), leading to an efficiency ratio of 77% in the quarter. This is not a good efficiency level and is much higher than the best banks in the U.S., which are below 60%, showing that Comerica’s top-line momentum is impacting quite negatively its fundamentals.

On the other hand, its asset quality remains excellent despite its relatively high exposure to commercial customers and some exposure to commercial real estate, showing that its underwriting criteria is sound, and credit losses should remain low in the near future. Despite that, its net income in the quarter was only $138 million, a decline of 57% YoY, and its return on equity (ROE) ratio was 9.3% (vs. 24% in Q1 2023).

Going forward, the bank’s operating performance, according to analysts’ estimates, is not expected to improve much in the coming quarters with net interest income expected to be around $2.2 billion in 2024 (-12% YoY) and its net income should drop to less than $700 million in the year (-22% YoY). This means Comerica’s financial performance is not particularly impressive in the short term, despite the “higher for longer” rate environment.

Given that the bank is highly exposed to rates, if the Federal Reserve eventually starts to cut interest rates in the coming months, Comerica’s business will certainly be impacted and its decline in revenues and earnings could be even worse.

While the bank hedges to some extent its exposure to rates through interest-rate swaps, its sensitivity to rates is still significant and Comerica’s top-line is likely to be pressured by the end of 2024 or 2025, if rates decline as expected nowadays by the street. Investors should not that current consensus is for the Fed to

Detroit, Michigan – Comerica Incorporated, a regional bank headquartered in Dallas, continues to face challenges despite offering a high dividend yield. Known for its focus on interest rates, the bank’s operating performance has been underwhelming, leading to a decline in its share price over the past year. Comerica’s business spans across multiple states, with a significant presence in Texas, California, and Michigan, as well as international operations in Mexico and Canada. While the bank boasts total assets of around $85 billion, making it a relatively ... Read more

San Francisco, California – Heron Therapeutics, Inc. has been in the spotlight recently for its advancements in medical technology. The company, known for its opioid-free surgical pain relief product, has seen significant growth in its stock price, with a 170% gain for investors who took a chance back in July 2023. However, despite this success, some reservations remain about the company’s operations. In a recent analysis, concerns were raised about Heron’s ability to live up to the potential of its products, highlighting the need for ... Read more

New York City, NY – As the fall season approaches, Americans are being advised to prepare for new Covid shots recommended for individuals 6 months and older. The Food and Drug Administration (FDA) has urged vaccine manufacturers to develop boosters targeting the KP.2 strain of the virus. This recommendation comes as the Centers for Disease Control and Prevention (CDC) advisors suggest updated Covid vaccines for those aged six months and above. The FDA has announced a strategic plan for autumn, focusing on the latest health ... Read more

New York, USA – The small biotech sector has faced significant challenges in 2024, trailing behind major indices such as the NASDAQ and S&P 500. Despite the overall market growth, the SPDR® S&P Biotech ETF has only seen a modest increase of around three percent this year, with a substantial portion of gains driven by technology giant Nvidia Corporation. Looking ahead, the Federal Reserve’s decision to cut interest rates could potentially benefit the high beta sectors of the market, including the small biotech industry. Furthermore, ... Read more

New York – The Clough Global Equity Fund, a closed-end fund attractive to income-focused investors, boasts an impressive yield of 10.50%. Compared to its peers in the global equity category, this fund offers a higher return, making it an appealing option for investors seeking steady income. The fund focuses on equity securities, a significant advantage in the face of rising inflation levels that may not be accurately reflected in official reports. With inflation potentially eroding the value of fixed-income securities, equity holdings provide a better ... Read more

Austin, Texas – Apple’s recent development in artificial intelligence (AI) technology has garnered significant attention from investors on Wall Street. The company’s stock is currently trading at a level that suggests high expectations of a successful “supercycle,” with little room for additional growth. However, concerns have been raised about the stock’s valuation, as it is trading at 32 times its forward price-to-earnings ratio, double the historical average before the pandemic. Despite the positive reception to Apple’s AI efforts, challenges have arisen, particularly in the European ... Read more

Boston, Massachusetts – Chewy shares experienced a surge in trading activity after a prominent figure in the meme stock world, Roaring Kitty, shared an image on social media resembling the online pet food retailer’s logo. Keith Gill, also known as Roaring Kitty, has a history of influencing trading through cryptic messages and memes, notably with GameStop. The image shared by Roaring Kitty led to a momentary increase in Chewy shares by up to 34%, reaching $39.10. The fluctuation in Chewy’s stock price during Thursday’s trading ... Read more

New York, New York – The world of growth exchange-traded funds (ETFs) is vast and diverse, offering investors a myriad of options to consider. One such ETF that emerged in mid-2020 is the Fidelity Blue Chip Growth ETF (FBCG). With a portfolio size of $1.9 billion, FBCG focuses on over 200 established domestic stocks, predominantly large-cap companies. The fund’s primary goal is to identify growth stocks with strong business models, solid pricing power, competitive advantages, and capable management teams dedicated to driving earnings growth over ... Read more

New York, NY – The Valkyrie Trading Society, a group of analysts specializing in high conviction and lesser-known investment opportunities in developed markets, is positioning themselves for success in the current economic climate. With a focus on long-only investments, the team aims to provide non-correlated returns with limited downside risks. One of their primary initiatives, The Value Lab, offers members access to a portfolio with real-time updates, 24/7 chat support, global market news reports, feedback on stock ideas from members, monthly new trades, quarterly earnings ... Read more

Investors in Chicago, Illinois are closely monitoring market volatility as a significant trade moves closer to a breaking point. The VIX, a measure of market uncertainty, is showing signs of potentially rising sharply in the near future. This increase in volatility could have major implications for traders and the overall market. Market analysts are attributing the potential spike in volatility to a combination of factors, including geopolitical tensions, economic uncertainties, and the ongoing trade war between the United States and China. As trade talks between ... Read more